Looking Back at October

Source: BTN Research

The S&P 500 lost 6.8% in October 2018 (total return). It was the worst month in more than seven years (since the September 2011 loss of 7.0%). It was also the worst October since the index fell 16.8% in October 2008, the beginning of the global real estate crisis. The S&P 500 consists of 500 stocks chosen for market size, liquidity and industry group representation. It is a market value weighted index with each stock’s weight in the index proportionate to its market value

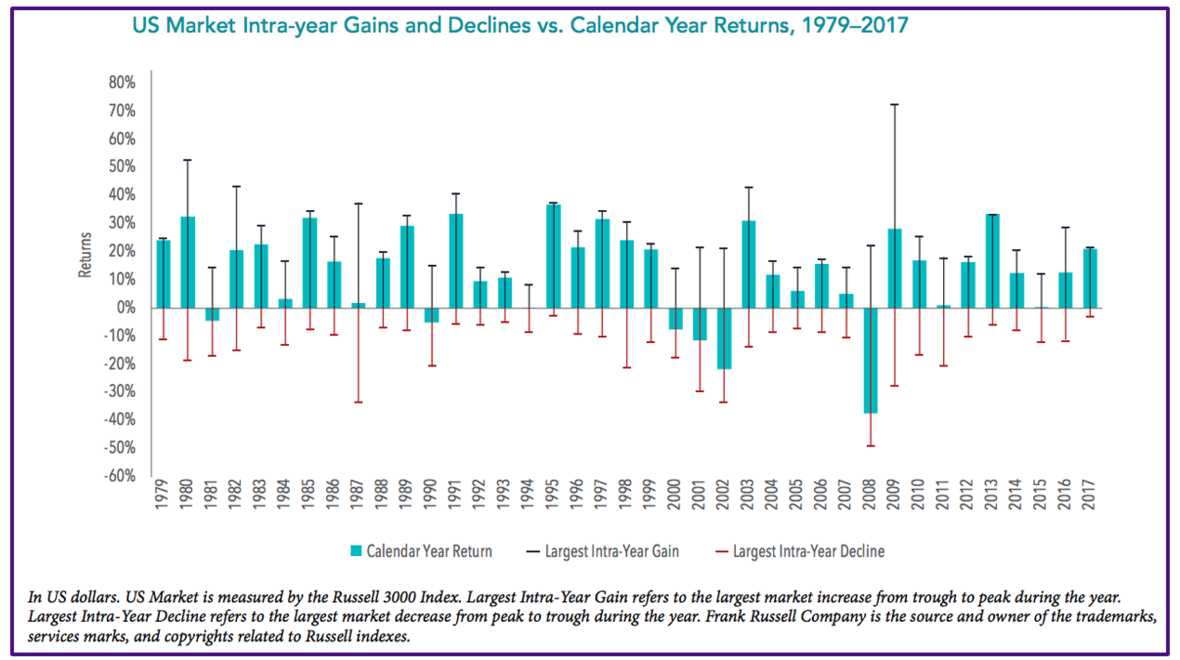

October was far from a pretty month for the market. It is important to keep in mind that although it was a painful month, it is not uncommon for the market to make a correction of possibly 10% once or twice a year.

The chart provides a historic visual that shows corrections every year. When looking at 2017, the correction was very small, comparatively speaking. This lack of volatility has some investors thinking that very little volatility is normal.

It is important to take a long term look at the market. Volatility in one month does not necessarily indicate how the market will react in the following months or finish the year.

Looking Ahead to November

As we begin November, it appears that U.S. stocks have begun to bounce back. There are a few things that could affect the market this month: the election, trade problems with China and the Federal Reserve’s decision regarding interest rates. We are cautiously optimistic that the market will end in positive territory.

Our View

We are keeping an eye on events that may influence the market, such as tariffs and short-term interest rates hikes, as well as the overall housing market. As investors, not traders, we need to look further into the fall and the end of the year. We still believe that our allocations should tilt away from bonds and outside the U.S exposure. We will continue to closely monitor economic developments, as well as global events that effect the market.